may 2025

// SDM Exclusive

Sponsored by:

SDM 100: Mixed, but Resilient

2024 was, by and large, an “average” year for many of the top 100 security dealers. But like seasoned chess players navigating a complex board, they still managed to find winning strategies despite the headwinds caused by external economic and geopolitical factors.

By Karyn Hodgson, SDM Editor

By all accounts, 2024 was a mixed bag for a number of SDM 100 companies. With high inflation/interest rates, and a turbulent election cycle, many companies reported average to below average results over the previous year.

“The market was weaker in 2024 compared to 2023,” wrote No. 6, Bay Alarm. “Elevated interest rates coupled with an election year put downward pressure on the market and negatively impacted customers’ willingness to spend.”

No. 23, HomePro Operating LLC, had similar observations: “We found 2024 to be flat over 2023. … Interest rates played a major factor in flat new construction starts. Existing housing was also impacted by interest rates as well as housing prices with inflation. This impacted homeowner moves in 2024.”

No. 42, Valley Alarm, described the market in 2024 as “about the same as 2023. CCTV and proactive video monitoring continued to be the strongest segments. … Inflation was problematic — margins were negatively impacted by price increases between the time of quote and time of install. The technical labor market was somewhat improved in 2024, but remained tight.”

No. 62, AES, noted: “Our market was slightly above average this past year as we generally saw some increased security spending. But on the opposite end, we had many customers cutting back due to uncertainty. At year end, after the election, our real estate developers and other similar customers started to pick up in demand compared to the beginning of 2024.”

Yet while in the individual responses, “uncertainty” was a common theme for many, as an aggregate, this year’s top 100 companies still did remarkably well — bringing in the highest total annual revenue in a decade, $17.4 billion. Both residential sales revenue ($706.7 million) and non-residential sales revenue ($3.2 billion) were up by double digits, 24 percent and 27 percent, respectively. Total RMR was down slightly, by 3 percent over last year, but was still the fourth highest number in a decade. Profits were also down just slightly, at 2 percent — with 56 percent of security dealers reporting an increase in profit margins in 2024, compared to 58 percent in 2023 — but were still above the 2022 number of 52 percent.

There is no one formula for how these companies excelled in the face of an “average” year for so many; but comments from those who cited a growth year give some insights.

“The market for security systems projects in 2024 proved strong compared to 2023, driven by robust growth in several key segments,” reported No. 98, Northeast Security Solutions Inc. “[We] experienced a 14.85 percent increase in overall gross income year over year, a testament to the sustained demand for our offerings and strategic improvements in operations. … In response to economic pressures like inflation and rising interest rates, we made strategic adjustments to protect margins and improve profitability. One significant initiative was enhancing our quoting accuracy to ensure that all billable hours were effectively captured. … While inflation elevated material and labor costs, our efforts to refine project estimates and deliver value to clients mitigated the impact. These improvements, alongside strong performance in growing segments like video and alarm equipment, allowed Northeast Security Solutions to not only navigate a dynamic market, but to emerge stronger in 2024.”

No. 71, Security Alarm Corp., called 2024 “very stable. We ended the year with about 10 percent growth compared to 2023. … One of our initiatives this year was to tap more into our existing customers. To try to stay ahead of inflation, we did raise rates about 7 percent at the beginning of 2024. We are doing another 4 percent increase at the beginning of 2025.”

No. 95, Pace Protection, credited a service culture with their growth. “The market was very strong in 2024 compared to 2023. There is an ever-increasing demand for safety and security. Our company was not impacted due to inflation or interest rates. There is a very high demand for companies that will provide exceptional service in an age where it is hard to get people on the phone.”

No. 93, Dallas Security Systems Inc. & DSS Fire, also wrote that they did not see much impact from inflation. “The market was strong and we saw good growth in video monitoring and cloud-hosted access control systems.”

No. 58, Prosegur Services Group Inc., best summed up the situation in its comments: “The market for security systems sales and integrated systems projects in 2024 experienced a mixed but largely resilient performance compared to 2023. While the demand for security solutions remained strong, economic factors such as interest rates and inflation influenced investment decisions across various sectors.”

This resilience is a key ingredient to the success of many of this year’s top 100 companies, who — like chess players responding to an unexpected move — were faced with major changes not just to technology but also to their markets. Read on for more comments on market shifts, technology trends and what they see ahead for 2025.

The market for security systems sales and integrated systems projects in 2024 experienced a mixed but largely resilient performance compared to 2023.

— Prosegur Services Group Inc.

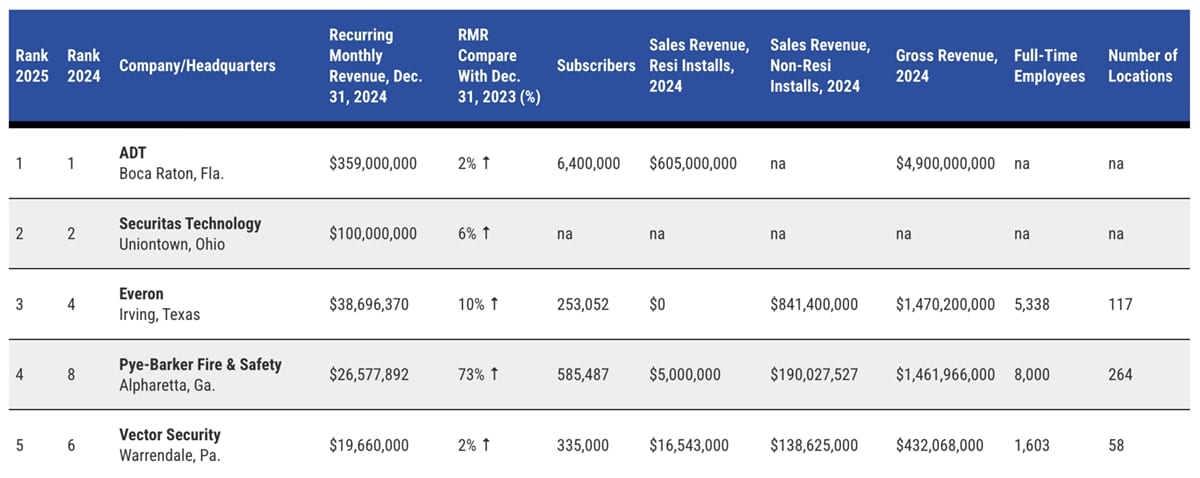

The table above presents aggregate figures for the SDM 100 group of companies, which are ranked by their recurring monthly revenue (RMR) — an industry standard of valuation of a security installation/monitoring business. Most of the SDM 100 companies are privately held. Submitting RMR is required for ranking; other figures are not required but mostly provided. Most companies — but not all — also reported their total annual revenue, number of subscribers, installation revenues, employees, and acquisition activity. Therefore, one should exercise caution in using this information to extrapolate industry totals or to benchmark. Note that some figures — such as total annual revenue, subscribers, and residential and non-residential sales revenue — fluctuate from year to year due to both acquisitions and inconsistent reporting by the ranked companies. Every effort is made by SDM to maintain consistency in reporting.

Market Shifts

Of the top 100 companies, about 60 percent of them sell residential systems, 73 percent commercial, and more than half sell both. But very few only sell residential these days, continuing a multi-year trend of residential security dealers getting more and more involved with commercial customers to mitigate competition from DIY, large national chains and other trends.

“We’ve seen an increased demand for commercial security solutions, driven by businesses requiring multi-system integrations that combine life safety, surveillance, access control and security technologies,” wrote No. 59, Advanced Security Systems. “This trend reflects the growing need for comprehensive, technology-driven security solutions across various industries. On the residential side, demand has remained stable without significant growth. While homeowners continue to prioritize security, the market hasn’t seen the same level of expansion as the commercial sector.”

No. 68, Security Systems of America (SSA), is one security dealer that has shifted its focus in recent years. “Our sales are increasing in the fire arena and commercial markets as we have moved our company to be better prepared for larger commercial projects involving video verification and focusing on school districts. … The DIY market has had the most noticeable impact on our residential market. Although we continue to support this market as it provides a solid base, many would-be customers consider the DIY options before a professionally installed system.”

This year, DIY came up frequently in the comments, along with other changes in how companies are approaching their business today.

“Competition for residential customers continues to be strong,” wrote No. 22, EMC Security. “Customers have many choices, including DIY. Many customers are moving to video-only solutions to reduce costs and false dispatch. Employee costs rose dramatically in 2024, with higher salaries and more expensive benefit packages. Coupled with this, the cost of materials, insurance and operating costs rose faster than any price increase to the customer. Customer acquisition costs also increased for residential customers. Commercial growth was strong. There was less price competition for commercial customers. … The security business is being redefined. Residential and small business consumers are increasingly comfortable with researching, selecting and installing their own security equipment and solutions. DIY, retail/internet offered products are replacing some of the market share formerly controlled by traditional dealers. … This has caused a movement of small/mid-sized alarm companies to move from a residential focus to a commercial systems focus.”

DIY is not just impacting the residential space, either. As No. 39, Habitec Security, noted, “DIY is crossing into the commercial space.”

The fire market was another one noted as being a place of opportunity for some of the top dealers. No. 30, Orr Protection, wrote, “The demand for advanced fire suppression, detection and monitoring solutions continued to rise as industries prioritized safety, compliance and asset protection. …. Macroeconomic factors, including interest rates and inflation, influenced project funding and capital expenditures. While some clients delayed discretionary upgrades due to higher borrowing costs; the essential nature of fire protection systems ensured steady investment in compliance-driven projects.”

No 51, Titan Alarm Inc., shared similar thoughts. “We are driving our business toward larger commercial installations and fire services because those are required for everyone.”

DIY, retail/internet offered products are replacing some of the market share formerly controlled by traditional dealers. … This has caused a movement of small/mid-sized alarm companies from a residential focus to a commercial systems focus.

— EMC Security

Recurring monthly revenue (RMR) in 2024 for SDM 100 companies declined 3 percent over last year, but remains the fourth highest in a decade. Fewer companies reported RMR growth in 2024 than in 2023, with 85 percent experiencing growth versus 91 percent last year. Out of all 100 companies, just 9 reported declines in RMR. Stand-out companies among the top 25 in RMR growth are: Pye-Barker Fire & Safety with 73 percent; Cook & Boardman with 37 percent; EyeQ Monitoring with 30 percent; and Elite ISI with 22 percent. Forty-one percent of the top 100 companies experienced double-digit percentage growth over 2023, with one — Visible Intellect LLC — reporting triple digit growth and another —Security 101 — reporting quadruple digit growth. Taking out those two, the average RMR growth experienced by the SDM 100 was 11 percent.

Technology Drivers

In addition to shifting market approaches, security dealers are also facing significant technology changes and demands for those solutions from their customers — particularly video solutions, as was also the case last year.

“We believe that the continued evolution and expansion of applications in the video space will result in a seismic shift in the industry,” wrote Mike McWilliams, president and chief operating officer of No. 3, Everon. “From video monitoring to video analytics and beyond, our customers are increasingly turning to us with business needs beyond surveillance that video can solve.”

No. 64, Custom Alarm, wrote: “This past year brought steady growth in certain system types, though overall performance remained average. One of the strongest areas of growth was the video surveillance sector, particularly in hybrid-cloud video management systems. We saw increased adoption across multiple verticals, including HOW, retail, and convenience stores. These solutions, combined with integrations between manufacturers, have also helped drive recurring revenue through video verification and live video monitoring services.”

While this trend is most prevalent on the commercial side, the residential sector is not immune. “In 2024 we continued to see consumer demand for home security cameras and this seems to reflect the fact that for video solutions and small business prospects, cameras have become ‘security,” wrote April Maloney, vice president, sales, for No. 8, Guardian Protection.

No. 43, Lifeline Fire & Security Inc., noted that proactive video monitoring is a very strong and high-growth market that will continue to be in demand for the foreseeable future, resulting in “the continued evolution of analytics and the associated impact of increasingly robust video monitoring solutions.”

AI and analytics are another sea change in the technology landscape top security dealers are seeing.

“AI has made it more attractive for us to sell a camera as an alarm trigger, so we foresee an ever-increasing market for this service, along with video footage to confirm an intrusion,” SSA wrote.

AI is a factor residentially as well. Guardian Protection’s Maloney sees both AI and DIY as technologies to watch going forward in the residential space: “In 2025, several key trends and challenges will impact Guardian Protection as an installing dealer with monitoring centers: AI-powered video surveillance and the continued rise of DIY, she wrote. “AI innovations for video will mean better proactive threat detection for the user, but integrating all of these innovations into monitoring services will require additional investment. The continued rise of DIY security systems and self-monitoring options will create further disruption as consumers increasingly opt for no-contract self-monitored solutions.”

And AI is also something top companies are starting to use for their own metrics to improve results.

No. 85, Haig Service Corp., wrote: AI — both generative and to an even great extent agentive — will be a revolutionary change and leveling up for those that focus on adoption and achieving/ realizing efficiencies. The ‘wide path toward happiness’ lies in the evolution from cheaper to more to BETTER (holy grail). We, for instance, have a clear corporate KPI for 2024 of achieving 40 percent improvement in efficiencies exclusively through leveraging AI and automation. To date we are well on our way and have already identified resulting definitive ROI.”

Politics may have a greater impact this year than in the past.

— Custom Alarm

Total annual revenue for the SDM 100 companies continued it’s climb, increasing by 7 percent, bringing it to the highest level in a decade.

Looking Ahead

There is no doubt about what is on everyone’s minds for 2025. As was also evident at ISC West in April, security dealers are concerned about tariffs. Writing comments in the first few months of 2025 (January-March), the SDM 100 companies mentioned the possibility of tariffs over and over again as a top concern for 2025 and beyond.

“The greatest impact on 2025 could be the impact of tariffs on security equipment and components that will likely drive up prices for end users, making security solutions less affordable across multiple sectors,” wrote Kevin Santelli, vice president commercial at Guardian Protection. “While demand remains strong, it may not be enough to fully offset rising costs, particularly for businesses and homeowners facing budget constraints.”

No. 24, Cook & Boardman Security Integration, wrote, “Tariffs have the potential to have the greatest impact in 2025. With the unknowns associated with them, the concern is that companies will hold off on making any investments until the picture becomes clearer. This will push projects out that are already awarded/planned and eliminate those that aren’t yet awarded.”

No. 29, General Security Inc. is already seeing some impacts, noting they were “seeing vendors pave the way for higher prices due to tariff concerns. Higher interest rates continue to be a drag on the residential side of our business.”

The political landscape will likely be a factor both positive and negative this coming year.

As Custom Alarm wrote: “Politics may have a greater impact this year than in the past. With a shift in power, we hope the government will ease regulations on small commercial security businesses, allowing us to better serve our customers. However, if interest rates remain high, they could continue to slow new construction projects, impacting demand for fire alarm and life safety systems. Additionally, changes in tariffs on electronic and security components entering the U.S. could affect our costs, a trend we are already noticing with some distributors.”

True to the resilient bunch they are, several companies pointed to opportunities as well as challenges.

“In the short term I see the fear of tariffs creating a potential drag on sales as people are figuring out what it means for their business, but I see us moving past that hopefully sooner than later,” wrote No. 41, Sonitrol Great Lakes/Solucient Security. “I see opportunity in providing solutions to the issues of active shooter/threat situations in both the education/government as well as the private sector markets. I am cautiously optimistic about the opportunities that AI can bring to the table to enhance the services we bring to our clients.”

No. 63, Cook Solutions Group, wrote that it looks at the security industry as a never-ending opportunity: “Tariffs, inflation, cyber threats and the increased use of AI will all have different impacts on the security business landscape. We see all of the above as opportunities for our company. We can often save our customers money by helping them become more efficient and gain new customers via this route as well. Most businesses NEED security so the budgets are there.”

Several companies mentioned the back to work initiatives being a potential driver this year.

“Continued return to office will drive the need for more/reconfigured spaces and security solutions,” wrote No. 76, Integrated Protection Services. “Tariffs have already impacted us, putting cost pressures on projects; we think a medium-term impact of that may be some on-shoring of manufacturing and industrial work.”

No. 82, Safe and Sound Security, took a different tack on the geopolitical front, and perhaps offers a guidepost for others as well.

“We’re going into 2025 with a big backlog so we’re expecting a growth year. We’ll invest even more in pursuing SLED projects and are expanding outside of California. We don’t focus much on the macro economy or politics to forecast. All we can do is focus inward and control what we can control.”

Objective of the SDM 100

The SDM 100 has been published since 1991. Its primary objective is to measure consumer dollars gained by security companies, in order to present an account of the size of the market captured by the 100 largest providers. SDM 100 companies are ranked by their recurring monthly revenue. RMR is the revenue associated with the contractual agreement between a security company and its subscriber — derived from customer billing for services such as monitoring, contracted service/system maintenance, security-as-a-service and managed/cloud solutions, and leasing of security systems — and is typically the basis for valuation of a security company. RMR is the language of security company executives and is meaningful in comparative analysis among industry peers. Of the 100 security dealers ranked, 32 of them earned more than $1 million in RMR in 2024.

How to Use the SDM 100 Tables

The 2025 SDM 100 ranks U.S. companies that provide electronic security systems and services to both residential and non-residential customers. This ranking is based on information provided to or, in few cases, estimated by SDM. Ranked companies were asked to submit either an audited or reviewed financial statement, or a copy of their income tax return showing total gross receipts for the stated period. The vast majority of the firms ranked are privately held.

The main table, ranks 100 companies by their recurring monthly revenue (RMR) of December 31, 2024. The company with the highest RMR is ranked as No. 1, and so on. For each of the 100 companies, the following information is provided, from left to right:

- Current year rank, which is based on Dec. 31, 2024, RMR.

- Prior year rank.

- Company name, as used in the marketplace (doing business as), and headquarters location.

- Amount of RMR billed on Dec. 31, 2024.

- Percentage of RMR increase/decrease compared with Dec. 31, 2023.

- Number of subscribers (recurring-billable customers) at year-end 2024.

- Amount of sales revenue from residential system installations in 2024.

- Amount of sales revenue from non-residential system installations in 2024.

- Total gross revenue, in calendar-year or (the company’s) fiscal-year 2024 from security system sales/installation, services, leasing, and monitoring.

- Number of full-time employees.

- Number of business locations, including headquarters.

SDM 100 companies are then re-ranked by several other criteria, including total annual gross revenue; residential subscribers; and non-residential sales revenue. See the report online at www.SDMmag.com/sdm100report for more data than presented here.

Note: An e following the figure indicates it is an SDM estimate.

To find a company by name, use the alphabetical index.

How to Purchase the SDM 100 Directory

Wouldn’t it be useful to have more information about each of the 100 companies ranked here? The 2025 SDM 100 Directory includes contact names, mailing addresses, telephone numbers, website URLs, branch office locations, product buyer names, installation data, and more. The SDM 100 Directory comes in Microsoft Excel format. To order, contact Jackie Bean at 215-939-8967 or by e-mail to beanj@bnpmedia.com.

background image / Sacura14 / Creatas Video+ / Getty Images Plus / via Getty Images